Frequently Asked Questions and Answers

- How do I get started?

- Who do I Contact for Problems and Assistance?

- What is a Super User?

- What is the Bulletin Board?

- What is a User?

- What is a User Profile?

- What is a Risk?

- What is a Panel?

- How is a Panel created?

- What is an Invitation?

- What are Alerts?

- How is a Risk created by a broker?

- How is a Risk Marketed by a broker?

- How is a Risk Panel created and how are Panellists invited to quote?

- How is a Risk edited?

- What is a Risk Identifier?

- How does an Underwriter quote?

- What is a Quote Identifier?

- What is a Dummy Quote?

- What is the Bidding Summary?

- What is Optimisation?

- What does it mean to ‘Close Out’ a Risk?

- How does Mail work?

- What is the Document Library?

- What are Templates?

- What can I do with Reports?

- What is the Event Log / History?

- Can my data / records be exported?

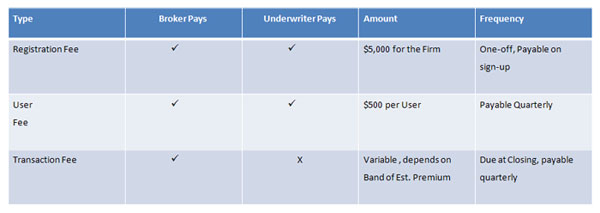

- What does it cost?

1. How do I get started?

The first step involves the RiskTrEx Administrator setting up an account (domain) for the firm and a Super User. The applying firm needs to submit an application to RiskTrEx containing confirmation of the firm's status as a bona fide insurance broker / adviser / agent or underwriter in their home country. This can be done via email (admin@risktrex.com) or from the web site. Approval takes no more than a few hours and results in the creation of a Firm's domain and Super User account (one per Firm in any location). The firm's account becomes active once the Terms & Conditions are accepted at first login by the nominated Super User.

2. Who do I Contact for Problems and Assistance?

You can contact admin@risktrex.com in the first instance. Once you have registered and have a User account, 'admin' is automatically added as a contact and can be mailed from the Messages (Create Mail) function.

3. What is a Super User?

A Super User is usually the Group Head or other senior manager with P&L responsibility for Users who will use the system. He is, however, able to see individual and aggregated User activity reports and can also take over any User's account. He need not be a technical person as his Super User role is simply to create User accounts.

At first log in, the Super User registers his contact information under 'Profile' and the firm's basic data, including the firm's logo for branding the firm's domain (and all Users' pages) under 'Firm Details'.

A Super User can switch into User mode and also has full rights to log in as any other User (whose account he administers) after which he can conduct a session using that User's account.

The Super User then creates individual User accounts for each person / broker who will use the system. He does this by giving the User a Username and Password which the User will reset after he has logged in.

4. What is the Bulletin Board?

It is a continuous information feed which is created and maintained by a Super User. It is useful because it generates scrolling announcements on the Home (landing) page of all Users under a firm's domain. A Super User can write a short message for broadcast to all Users who are able to see it immediately.

5. What is a User?

A User is typically a broker or underwriter employee of the firm who is authorised to do business on the platform from within his firm's domain. A single firm may have as many Users as they wish. An individual User account is first created by a Super User who sets up a unique Username and Password for the User. The Password needs to be reset by the User the first time he logs in.

6. What is a User Profile?

Every User must complete a two-part Profile ('Personal' and 'Business') before he can start using the platform. The Personal Profile contains basic personal and contact info. The Business Profile defines the type of business he is interested in transacting (e.g. business lines and geographical areas) and assists counterparties in deciding whether they wish to do business with the User by allowing him to join their Panel.

7. What is a Risk?

A Risk is created by a broker User. It specifies the requirements of a prospective policyholder for cover and forms the basis for an underwriter User to quote. Risks may be simultaneously saved as Templates and can be a useful starting point, avoiding rekeying, when creating new risks later.

8. What is a Panel?

A Panel is a group of Users who have been invited and have subsequently accepted the invitation to join another User's panel. Once registered, a User needs to set up his Panel if he wishes to do business on the Platform. It is a critical activity because only Panel members can be counterparties. Internal mail exchanges via the platform's messaging tool are possible only with other Panellists. Continuous review and updating of the Panel is recommended.

9. How is a Panel created?

The first step to create a Panel is to identify appropriate counterparties whose Profile fits with the type of business the User wishes to do. This is done via a system-wide search and identified candidates can then be invited to become Panel Members through the system's internal messaging capability Once acceptance has occurred, each party appears on the other's Panel and the counterparties can then transact business as well as mail each other from within the system. Adding an underwriter to a broker's Panel means that, when a transaction is being marketed by a broker, that underwriter will automatically be in the broker's list of potential recipients if the risk details match the underwriter's preferences which he created in his Business Profile. A party can also be removed from a Panel unilaterally.

10. What is an Invitation?

An invitation is a request either a) to join a User's Panel (only underwriters join brokers' Panels and vice versa) or b) to accept a broker's invitation (the recipient being an underwriter) to quote on a risk he has created and is marketing. The recipient accepts or declines the invitation with a single click and the sender is informed accordingly. Re-invitation is possible.

11. What are Alerts?

Alerts are system generated messages, their purpose being to inform the recipient that an 'event' has taken place. An 'event' could be a Panel invitation, Panel acceptance, a quote request or a quote submission etc. Alerts are not only useful to draw the recipient's attention to the 'event' but also frequently a call to action Alerts appear on a User's landing (home) page and are removed from the Home page once they have been read.

12. How is a Risk created by a broker?

A risk can be created from scratch or from a pre-existing template by a broker. There are three sections which need completion when creating a risk:

- Policy Holder Information - Information on the Policyholder (name may be withheld from underwriters).

- Risk Information - key policy data including the policyholder's required sums insured (limits) and estimated projections for turnover, deductible etc.

- Supporting Documents - Document files created outside the system (such as Word, Excel or pdf documents etc.) which the broker wishes to send to underwriters to assist in understanding and quoting for the risk. These can be uploaded and 'attached' to the risk.

In Risk Information the Broker creates must enter a cut-off date (Quote Deadline) by which underwriters must submit their quote for it to be considered and this must be before the Risk Start Date, another mandatory field. It is usual for Brokers to set the Quote Deadline to be some time (usually several weeks) before the renewal date for existing risks or Start Date for new risks so that there is sufficient time for a review of the quotes and structuring the insurance contract with the input of the policyholder. This can be edited if circumstances change and, as with any amendment (edit) of a risk, an alert is immediately sent to all underwriters on the Risk Panel.

The system stores all risks created indefinitely and risk data can be deleted and exported at will.

13. How is a Risk Marketed by a broker?

Risk marketing is a three stage, sequential process: 1) Create Risk, 2) Create Risk Panel and 3) Invite underwriters to quote. Each stage is carried out independently to give the broker the opportunity to edit and review his placement strategy.

Whether it is a coinsured or single insurer situation, obtaining competitive quotes from underwriters is the key task when placing a risk and this requires marketing it. First the risk needs first to be created on the RiskTrEx platform. Following that, it is necessary to create a Risk Panel of underwriters who are to be invited to quote. Assuming that the broker has already populated his (main) Panel with one or more underwriters, they will appear as potential invitees if they match. Importantly, non-panel underwriters who also match the risk are also identified for invitation to the Panel, and from there the Risk Panel. The final step for the broker is to issue invitations to underwriters and this allows them access to Policyholder and Risk information as well as uploaded broker presentations in order that they have the required information to quote on a particular Risk.

14. How is a Risk Panel created and how are Panellists invited to quote?

Creating a Risk Panel involves selecting the active Risk which is ready to be sent to underwriters and searching for underwriters whose underwriting criteria (defined in their Business Profiles) match the characteristics of the Risk. Three categories are listed:

- Risk Matched Underwriters - underwriters who are on the Panel and match the risk parameters. They can now be invited to receive an invitation to quote for the Risk with a single click (which they can accept or decline). Upon invitation, an alert is sent to the underwriter and the underwriter is marked as 'pending'. Should he accept, he is added to the Risk Panel and may submit his quote at any time up to the Quote Deadline.

- Risk Matched Non Panellist Underwriters - underwriters who are not yet on the Panel but match the risk parameters are also automatically identified. This category is particularly important as it catches underwriters who are not on the broker's Panel but who have stated that the particular risk meets their underwriting criteria. These underwriters need to become Panellists (through invitation and acceptance) first so that they can then be invited to quote and so an option to invite them to the main Panel is offered.

- Non Risk Matched Underwriters - underwriters who are on the Panel but do not match the risk parameters. This category of underwriters is not suitable to approach as the Risk does not fit their underwriting preferences.

Only one User from a Firm is allowed to be on a Risk Panel and quote for a Risk to avoid inadvertent competition among Users within a firm.

15. How is a Risk edited?

A risk can change during the marketing period such as when new information becomes available. Amending a risk is possible at any time and any amendment made to a Risk by a broker results in an alert being sent to all Risk Panel underwriters who are requested to resubmit their quotes, taking into account the new information. Any time a risk is changed, each version of that risk is retained (tagged with a unique 'Risk Identifier') together with a record of all 'events' (quotes etc.) associated with that Risk, including version identification for compliance purposes.

16. What is a Risk Identifier?

A Risk Identifier is a RiskTrEx generated reference number which is unique and contains information about the broker who created it, the office / location from where he operates the date of creation and the version number. Users will become familiar with the structure after some time.

17. How does an Underwriter quote?

Sending a quote to a broker is possible only after an underwriter has accepted an invitation to be on a Risk Panel. This allows him access to all the risk data posted by the broker (the Policyholder's name may be withheld) including uploaded supporting documents (Word, Excel, pdf etc.) from which to evaluate the risk, propose pricing and coverage terms.

The underwriter starts by deciding whether to accept the broker's proposed terms in full. By doing so, he limits the fields he can alter to those not suggested by the broker. To assist with negotiations and contract formation, the underwriter may identify price sensitive terms, these being terms he is, in principle, willing to negotiate on. In addition to pricing and deductible, the underwriter must specify whether he is interested in being lead underwriter and the % of the total exposure he can take on the quoted terms. Other elements of the quote which need to be specified include whether the quote is net of broker commission and whether profit share is offered.

18. What is a Quote Identifier?

A Quote Identifier is a RiskTrEx generated reference number which is unique and contains information about the underwriter who created it, the office / location from where he operates the date of creation and the version number. Users will become familiar with the structure after some time.

19. What is a Dummy Quote?

A broker User may add a Dummy Quote to the pool of quotes on each Risk. This permits quotes received from outside the system to be included when using Optimisation and other tools.

20. What is the Bidding Summary?

The bidding summary gives the broker an up-to-date status report of the number and type of quotes received for a Risk as well as the high and low pricing submitted by underwriters. It is possible for the broker to switch on (and off) the display of some or all of these fields to underwriters who are on the Risk Panel. This can be used to enhance competition by giving non-specific quote / pricing information anonymously.

21. What is Optimisation?

Where a large number of quotes are submitted for varying percentages of a given risk (as is the case with coinsured placements), there are often many combinations of underwriters which achieve 100% coverage for the policyholder. Optimisation is a tool which assists the analysis and ranking of quotes received for a risk. The tool helps with building the underwriting syndicate comprising one 'lead' insurer followed by other underwriters who 'follow', with each firm pricing its own share at the price it quoted. Optimisation produces two results: the absolute least cost solution and the least cost solution with the constraint of using the fewest Underwriters.

22. What does it mean to 'Close Out' a Risk?

Once a risk has been concluded, whether through a successful placement or not, it needs to be 'Closed Out' to be removed from the active screens. This sets up the syndicate structure in terms of % line underwritten by each archives it and adds it to the database used for analysing historic business activity. It also generates the Transaction Fee based on the estimated premium for the subscribed policy.

There are three ways to 'Close Out' a Risk. As the system offers an 'Optimisation' tool which ranks and finds the optimal syndicate based on lowest cost and fewest underwriters, these are suggested as default solutions. The User can also close out in two additional ways: 1) based on a 'customised solution' or 2) as 'unresolved'. The results of a 'Close Out' can be printed or exported for use by back office / operations colleagues to generate final documents.

23. How does Mail work?

The system has an internal e-mail capability which can also be configured to send copies to an external e-mail account. A User can only exchange e-mail with Users on his Panel. Mail is stored indefinitely and the User has the standard email functions available to him.

24. What is the Document Library?

It is a tool which allows documents to be uploaded, stored and accessed from within the User's domain. Documents are tagged either as only for the User's personal use or for public use (i.e. by any User, panellist or not). A User can view, download and use public documents uploaded by other Users, i.e. policy terms and conditions, key clauses, newsletters, press releases, articles, presentations etc.

25. What are Templates?

Templates can save time and effort in populating the fields required to create or quote for a risk: particularly standard clauses, policy wordings and definitions used in an insurance contract which do not vary often. At the end of the form for creating a risk or a quote, the User has an option to also create a Template from the data he has input for future retrieval and use. He does so by saving as a Template and giving it a memorable name. Thereafter, it can be retrieved and used to create a risk or another template. It is also possible to simply create a new Template.

26. What can I do with Reports?

This is the section from which Users can generate activity and business analysis reports. Sorting and filtering records is possible so that user-defined reports can be created, printed and exported for analysis and review.

27. What is the Event Log / History?

The database captures every 'event' (quote, amendment etc.) for every Risk created on the platform. These can be filtered, sorted, viewed and exported providing a powerful compliance tool.

28. Can my data / records be exported?

A copy of a Users data can be exported and made available to a Super User. This is only possible with a signed, written instruction of the firm's Super User which has been countersigned by a Board Director or person of similar standing. It can only be done by the RiskTrEx System Administrator for security reasons.